Sxcoal Issue 31# | China coking coal extends fall; met coke downside risk grows

China's coking coal market extended downward trend last week, while met coke market stabilized temporarily but lacked support...

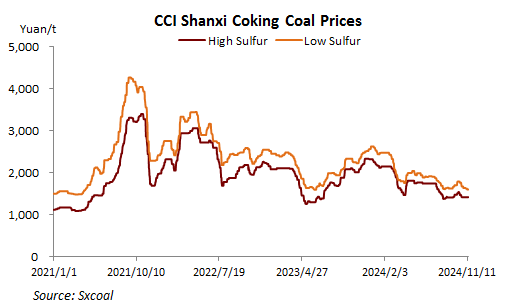

Coking Coal

Market Overview: China's coking coal market experienced a continued downward trend last week due to weak demand. Steel and coke producers purchased coking coal only as needed, leading to stagnated sales and inventory pressures, which in turn led to sustained price drops.

Supply and Demand: The supply of coking coal increased as some mines resumed operations, and there was a slight production increase at a few mines. However, weak demand for finished steel during the traditional lull resulted in prolonged coke price cuts. Coking plants prioritized digesting existing feed coal stocks, maintaining low coal inventories, and made only necessary purchases.

Inventory: Coking coal stocks at 100 surveyed coking plants could sustain 6.16 days of usage, a decrease of 0.08 day from the previous week. Raw coking coal stocks at surveyed mines reached 3.03 million tonnes as of November 13, up 3.06% on the week, while washed coal stocks increased by 4.57% from a week ago to 2.29 million tonnes.

Prices: Coking coal prices trended downwards in most parts of Shanxi. Low-sulfur fat coking coal fell by 50 yuan/t to 1,500 yuan/t, with a cumulative reduction of 250 yuan/t since mid-October. Online auctions faced high failure rates, especially for high-priced cargoes.

Mongolian Coal: Mongolian coal transactions were sluggish, with prices persistently moving lower. The prices for Mongolian 5# raw coal under long-term contracts declined by 30 yuan/t to 1,100-1,110 yuan/t, ex-stock Ganqimaodu with VAT. The daily throughput at Mandula port increased, but downstream buyers mostly held back on purchases, depressing trading activity.

Seaborne Imports: In the seaborne import market, participants adopted a wait-and-see approach due to flat overseas demand. Australian coal prices were largely stable with minor adjustments. Australian premium hard coking coal offers were temporarily at $206/t FOB, or 1,840 yuan/t CFR China with VAT, indicating no pricing advantage over domestic equivalents, leading to cautious procurement among Chinese traders.

More details in our latest weekly coking coal review, incl. our weekly survey on coking coal mines, market dynamics, etc. »CLICK HERE

Met Coke The Chinese metallurgical coke market experienced a temporary stabilization last week but lacked support from costs and demand. The market sentiment was dampened by weaker-than-expected reactions following a key government meeting and by Northern China steelmakers’ request for a third round of price cuts for the material.

Coke production remained high, with capacity utilization at Sxcoal-surveyed coking plants increasing slightly to 82.3% last week. However, environmental inspections led to a slight retreat in regional coke supply.

Steel mills controlled coke arrivals due to reduced molten iron output and squeezed margins from falling steel prices, leading to continued stock accumulation at surveyed coking plants, which climbed for the fourth week to 589,600 tonnes (+ 9.9% WoW).

More details in our latest weekly met coke review, incl. our weekly survey, market changes and updates on domestream sectors. »CLICK HERE