Sxcoal Issue #11 | Weekly review of Chinese coal market

This is a weekly review of the Chinese coal market -- thermal coal, coking coal and met coke, based on our exclusive surveys and analysis.

If you’re already subscribed and/or like this free newsletter, hitting the LIKE button is one of the best ways to support our work.

Thermal coal

China's thermal coal market rebounded last week after two weeks of decline, as some end users started to take advantage of the low prices to restock. Yet, trading liquidity remained subdued and end buyers still frowned on prices.

On February 20, 5,500 Kcal/kg NAR thermal coal traded at Qinhuangdao port was assessed at 1,030 yuan/t FOB with VAT, up 16 yuan/t from February 17. The 5,000 Kcal/kg NAR grade was assessed at 867 yuan/t, up 18 yuan/t from late last week, and the 4,500 Kcal/kg NAR grade was assessed at 750 yuan/t, a 10 yuan/t rise.

The uptrend in China’s domestic market also helped stabilizing Indonesian thermal coal prices, especially at a time of low quantities of mid- and low-CV coals held by traders.

Chinese utilities raised their tender prices for seaborne coal purchases. The lowest awarded price in early days of last week was 561 yuan/t DDP with VAT, basis 3,800 Kcal/kg NAR, but increased to 585 yuan/t in late days, with the netback price up by $1-2/t from $65-66/t to $67-68/t FOB.

On February 20, the Fenwei CCI 4700 Import index stood at $99.5/t CFR, up $2.5/t from the pre-holiday level; the Fenwei CCI 3800 Import index was $77/t CFR, a $2.7/t fall.

Coking coal

China's coking coal market remained largely steady yet weak last week, as downstream sectors still had little interest in purchases. Coal stocks at mines had increased for three consecutive weeks, and some mines with large inventory pressure continued to lower offer prices.

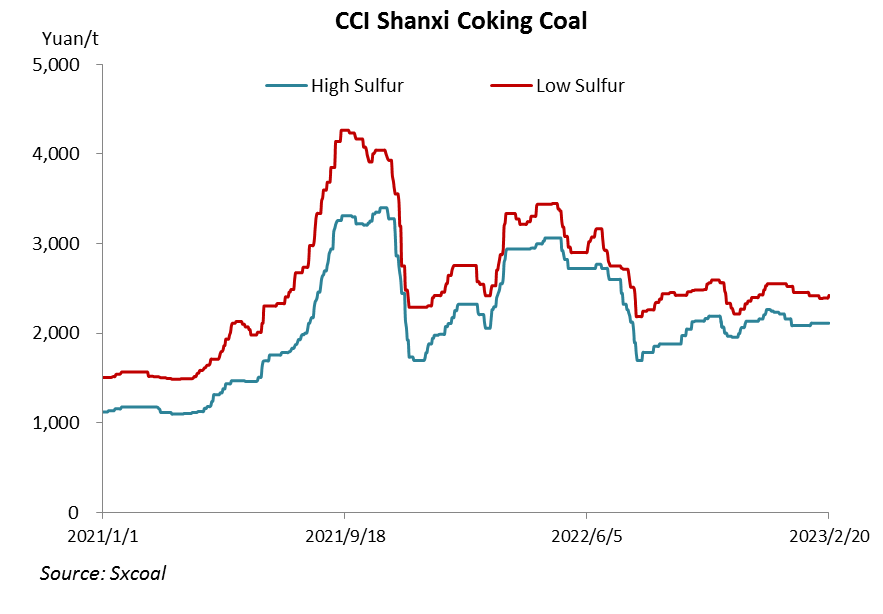

The Fenwei CCI Index for Shanxi low-sulfur primary coking coal rose 4 yuan/t from a week ago to 2,392 yuan/t on February 17, ex-washplant with VAT; and the index for Shanxi high-sulfur primary coking coal unchanged at 2,112 yuan/t.

By contrast, offer prices for Australian premium coal continued to leap higher during last week. HCC prices rose to $405/t FOB on February 17, up $35/t week on week. Some coke makers and traders started to make moderate purchases, but deals closed were small.

China is expected to see more Australian coking coal imports in the coming month as the direction of improving trade ties between the two countries becomes clearer, as indicated by a spokesperson with China's Ministry of Commerce as well as feedbacks Sxcoal has received from market participants.

Met coke

China's metallurgical coke prices were steady as a whole last week. Coke supply moderately rebounded yet demand little improved, resulting in higher coke inventories at both coking plants and steel mills and adding to the downside pressure.

Mills continued to make on-demand purchases amid steady rebound of steel production, yet some still limited daily intakes due to high inventories.

Sxcoal's tracking data showed the capacity utilization of blast furnaces in surveyed mills increased 1.12 percentage points week on week to 79.54% in the week ending February 17.

The overall capacity utilization at the coking plants surveyed by Sxcoal inched up 0.71 percentage point week on week to 78.14% and coke output climbed 0.9% week on week to 2.77 million tonnes in the week ending February 16.

Fenwei assessed the price of Grade II met coke (0.8% sulfur, 13.5% ash, CSR 55) at 2,540 yuan/t with VAT, DDP Tangshan, flat week on week. Grade II met coke (0.8% sulfur, 13.5% ash, CSR 55) was assessed at 2,500 yuan/t in Rizhao, DDP basis with VAT, also unchanged compared with the week-ago level.

The above articles are also included in our China Coal Weekly newsletter sent to paid subscribers via email each Monday. Download a recent SAMPLE?